Table of Contents

- What Is Covered by Flood Insurance Policy: An Overview

- Building Property Coverage Under Flood Insurance

- Personal Contents Coverage in Flood Insurance Policies

- Flood Insurance Exclusions: What Is Not Covered

- Does Homeowners Insurance Cover Flooding or Flood Damage

- NFIP vs. Private Flood Insurance: Coverage Comparison

- Flood Insurance Waiting Period and Policy Activation

- How to File a Flood Insurance Claim: Step-by-Step Process

What Is Covered by Flood Insurance Policy: Complete Guide

Last Updated: July 8, 2026

When a flood strikes, standard homeowners insurance typically won’t cover the damage. Understanding what is covered by flood insurance policy is essential for protecting your home and belongings in Las Vegas and throughout Nevada. According to FEMA data, flooding causes billions in annual property damage across the United States, yet many homeowners remain underinsured for this specific risk.

What Is Covered by Flood Insurance Policy: An Overview

Flood insurance provides protection against direct physical damage caused by floodwaters. This coverage is critical because most standard homeowners policies explicitly exclude flood damage. The National Flood Insurance Program (NFIP), administered by FEMA, is the primary source of flood insurance for most American homeowners.

What is covered by flood insurance policy includes structural damage to your building, certain systems and utilities, and some personal property. Replacement cost coverage is typically available for building property, meaning you can rebuild or repair your home without depreciation. Personal property coverage may be available on an actual cash value basis, which accounts for depreciation over time.

Check your flood zone designation through FEMA’s flood map service. Even properties outside high-risk zones can experience flooding, and lenders may require coverage if your home is in a mapped floodplain.

Understanding the National Flood Insurance Program

The National Flood Insurance Program was established in 1968 to provide flood coverage when private insurers wouldn’t. Today, NFIP serves as the backbone of flood insurance in the United States, offering policies through participating insurance agents and companies. NFIP policies come in two main types: standard policies for residential buildings and contents, and preferred risk policies for properties in lower-risk areas. The program sets standardized rates based on flood zone designation, elevation, and building characteristics, ensuring coverage remains available across all risk levels.

Many Las Vegas residents benefit from NFIP’s predictable pricing structure and broad availability. The program covers both the building structure and personal contents, though you must purchase these coverages separately.

Direct Physical Damage from Floodwaters

Direct physical damage from floodwaters is the core coverage provided by flood insurance. This includes structural damage to your home’s foundation, walls, roof, and interior systems caused by standing water or flowing water from a flood event. The definition of a "flood" under NFIP includes overflow of inland or tidal waters, unusual and rapid accumulation of runoff, and mudslide where it results from flooding.

When floodwaters enter your home and cause damage, your flood insurance policy covers the cost of repairs or replacement up to your coverage limits. This includes damage to built-in appliances, flooring, drywall, electrical systems, and HVAC equipment. Damage from water that backs up through your plumbing system during a flood is covered only if you purchase the optional sump pump overflow endorsement.

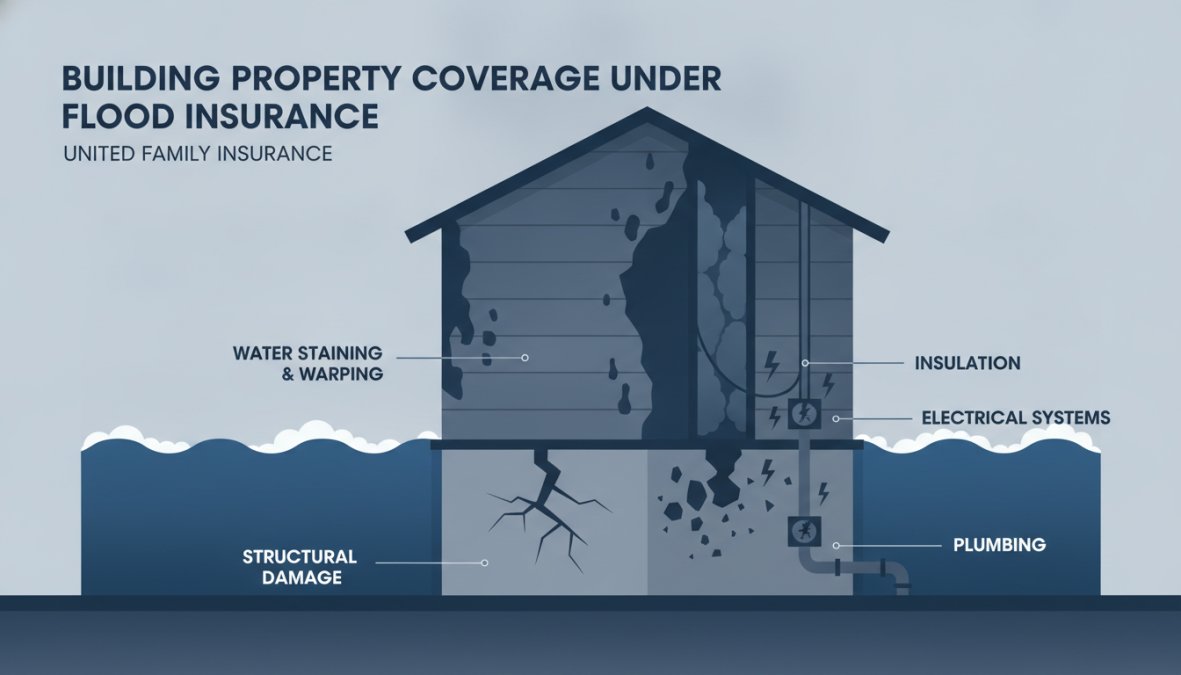

Building Property Coverage Under Flood Insurance

Building property coverage protects the structure of your home, including the foundation, walls, roof, and permanently installed systems. Coverage limits for building property typically range from $250,000 to $500,000 under NFIP standard policies, though higher limits are available through excess flood insurance. Your deductible applies to each flood event, with common options ranging from $500 to $5,000.

Structural Damage and Foundation Protection

Structural damage is where flood insurance provides its most critical protection. When floodwaters enter your home, they can compromise the integrity of your foundation, weaken load-bearing walls, and damage the overall structural system. Flood insurance covers the cost of stabilizing and repairing these structural elements, which are often the most expensive components of flood recovery. Foundation repairs can cost tens of thousands of dollars, and flood insurance covers damage to concrete slabs, basement walls, pilings, and other foundation components caused by direct physical loss from flooding.

Basement walls are particularly vulnerable to flood damage. Water pressure against basement walls can cause them to crack or collapse. If your home has a basement, ensure your building coverage limits are sufficient to address potential structural repairs.

Systems and Utilities

Permanently installed systems and utilities are covered under building property coverage. This includes electrical systems, HVAC equipment, water heaters, plumbing fixtures, and appliances that are built into the structure. Your electrical panel, wiring, outlets, and switches are covered if damaged by flooding. Similarly, heating and cooling systems, water heaters, and furnaces are included in building coverage. Permanently installed kitchen appliances like dishwashers and ovens are covered, but portable appliances may fall under personal property coverage instead.

Personal Contents Coverage in Flood Insurance Policies

Personal contents coverage protects your belongings, furniture, clothing, electronics, and other household items from flood damage. This coverage is optional, though highly recommended for most homeowners. Coverage limits typically range from $5,000 to $100,000, depending on your policy and the amount of coverage you select.

Personal contents coverage operates on an actual cash value (ACV) basis under standard NFIP policies. This means your reimbursement is reduced by depreciation based on the age and condition of each item.

What Personal Belongings Are Covered

Most household items are eligible for personal contents coverage under a flood insurance policy. Furniture, bedding, clothing, shoes, books, and electronics are typically covered. Kitchen items, including pots, pans, dishes, and small appliances, are included. Sporting equipment, tools, and hobby supplies are generally covered as well.

Important documents and valuables have specific coverage limits. Cash, coins, and precious metals typically have a maximum coverage limit of $2,500. Jewelry, watches, and furs are limited to $2,500 as well.

Coverage Limits and Replacement Cost

Personal contents coverage limits determine the maximum amount your insurer will pay for damaged belongings. Replacement cost coverage is available through some private flood insurance carriers, reimbursing you for the cost of replacing items with new equivalents without deducting for depreciation.

To maximize your coverage, maintain an inventory of your personal property. Photograph or video-record items in each room, including furniture, electronics, and decorative items. Store this inventory in a safe location, such as a cloud storage service or safe deposit box.

An inventory of your personal property is your best defense in a flood claim. Itemize what you own, note the approximate value, and store photos or video in a secure location. Without documentation, proving your losses becomes significantly more difficult.

Flood Insurance Exclusions: What Is Not Covered

Understanding what is not covered by flood insurance policy is as important as knowing what is covered. Flood insurance does not include damage from water that backs up from your sewer or drain system, unless you purchase the sump pump overflow endorsement. Damage from poor drainage, seepage, or gradual water infiltration is typically excluded. Flood insurance also excludes damage from waves, storm surge, or water that travels across land as a result of waves. Additionally, damage to the land itself, erosion, settling, or loss of soil, is not covered.

Basement-Specific Exclusions and Limitations

Basements present unique challenges for flood insurance coverage. While personal contents in your basement are covered, coverage for the basement structure itself has specific limitations. Under NFIP standard policies, coverage for basement improvements is limited to a maximum of $5,000 per policy. This means if you have a finished basement with drywall, flooring, and built-in storage, your total coverage for these improvements is capped at $5,000 regardless of the actual replacement cost.

Basement flooding is common in Las Vegas during heavy rainfall events and monsoon season. If your home has a basement, consider excess flood insurance to supplement your NFIP coverage.

Common Exclusions You Should Know

Several common exclusions apply to all flood insurance policies. Damage from wind, hail, or lightning is excluded because these are covered under homeowners insurance. Damage to vehicles is excluded from flood insurance. Property outside your home is generally excluded, including landscaping, trees, shrubs, fences, decks, and patios. Temporary housing and living expenses are not covered by flood insurance.

Does Homeowners Insurance Cover Flooding or Flood Damage?

Standard homeowners insurance policies explicitly exclude flood damage. This exclusion applies to all types of water damage caused by flooding, regardless of the flood’s source or severity. Homeowners insurance does cover water damage from other sources. If a pipe bursts inside your home or a storm damages your roof and rain enters, homeowners insurance covers the resulting water damage. The key distinction is that homeowners insurance covers water damage from sources other than flooding.

Why Separate Flood Insurance Is Necessary

Separate flood insurance is necessary because homeowners insurance simply does not cover flood damage. Even if you have comprehensive homeowners coverage, you have zero protection against flooding without a separate flood policy. This gap in coverage can be financially devastating if your home experiences flood damage.

Flood insurance is available through the National Flood Insurance Program and through private carriers. NFIP policies are standardized and available to most homeowners, regardless of flood risk. Private flood insurance carriers offer additional options, including higher coverage limits, replacement cost coverage, and broader coverage terms.

If your mortgage lender requires flood insurance, you must maintain continuous coverage. Lenders typically require proof of active flood insurance annually. Allowing your policy to lapse can result in forced placement coverage, which is significantly more expensive than standard flood insurance.

NFIP vs. Private Flood Insurance: Coverage Comparison

The National Flood Insurance Program and private flood insurance carriers offer different coverage options and pricing structures. NFIP policies offer standardized coverage and rates based on flood zone designation and building characteristics. Private flood insurance carriers offer more flexibility in coverage options and higher limits. Replacement cost coverage is more readily available through private carriers, and coverage limits can exceed NFIP maximums.

| Coverage Aspect | NFIP Standard Policy | Private Flood Insurance |

|---|---|---|

| Building Coverage Limit | Up to $500,000 | Up to $2,000,000+ |

| Contents Coverage Limit | Up to $100,000 | Up to $500,000+ |

| Deductible Options | $500-$5,000 | $500-$10,000+ |

| Coverage Basis | Actual Cash Value | Actual Cash Value or Replacement Cost |

| Basement Improvements | $5,000 maximum | Often higher or no limit |

| Availability | All properties | Risk-based underwriting |

Excess Flood Insurance and Additional Protection

Excess flood insurance provides additional coverage limits above your primary flood policy. This supplemental coverage is particularly valuable if you have a high-value home or significant personal property that exceeds your primary policy limits. Excess flood insurance typically applies only after your primary policy limits are exhausted. For properties in Las Vegas with significant value or those located in flood-prone areas, excess flood insurance is a prudent investment.

Flood Insurance Waiting Period and Policy Activation

Flood insurance policies have a waiting period before coverage becomes effective. The standard waiting period for NFIP policies is 30 days from the policy inception date. During the waiting period, your flood insurance policy is in force, but coverage for losses caused by flooding does not apply. The only exception is if your policy is a renewal or replacement of prior flood insurance with no lapse in coverage.

Timing your flood insurance purchase strategically helps you avoid gaps in coverage. In Las Vegas, the monsoon season typically runs from June through September, so purchasing coverage by May ensures you’re protected well before peak flood risk.

How to File a Flood Insurance Claim: Step-by-Step Process

Filing a flood insurance claim requires careful documentation and adherence to specific procedures. Contact your insurance agent or carrier immediately after flood damage occurs. Provide notice of your claim as soon as possible, ideally within 24-48 hours of the flood event. Your insurer will assign a claims adjuster to assess the damage, inspect your property, and document the extent of loss.

Document all damage with photographs and video before cleanup begins. Take pictures of damaged areas, destroyed items, and the water line showing how high floodwaters rose in your home. Create a detailed list of damaged items, including descriptions and approximate values.

Documentation and Proof of Loss

Proof of loss is a formal statement documenting the damage to your property and the amount of your claim. Your insurer will provide a proof of loss form that you must complete and submit. Gather receipts, invoices, and other documentation proving the value of damaged items. For structural damage, obtain repair estimates from licensed contractors. Keep copies of all documents you submit to your insurer and maintain a record of dates, times, and names of people you communicate with regarding your claim.

Do not discard damaged items or begin major cleanup until your adjuster has inspected the damage. Your insurer may want to examine damaged items to verify the cause of loss. Premature cleanup can result in claim denials if your insurer cannot verify the damage.

Post-Flood Mitigation Requirements

After a flood, you have a responsibility to take reasonable steps to mitigate additional damage. Mitigation means taking actions to prevent further loss or damage to your property. Common mitigation actions include removing standing water, opening windows to promote drying, and removing saturated materials like drywall and flooring. You should also turn off utilities if it’s safe to do so and remove items from standing water to prevent additional damage.

Your insurer may deny coverage for damage that results from your failure to mitigate. Document your mitigation efforts with photographs and notes about what you did and when. Save receipts for any mitigation materials or services you purchase.

Flood damage can strike unexpectedly, leaving homeowners facing tens of thousands of dollars in uninsured losses. Understanding what is covered by flood insurance policy ensures you have the protection your home and belongings deserve. Contact United Family Insurance today to get a personalized flood insurance quote and protect your most valuable asset from the financial devastation of flood damage.

Frequently Asked Questions

What is covered by flood insurance policy if I have a basement?

Flood insurance covers structural damage to your basement from direct physical damage caused by floodwaters, including foundation repair and water removal. However, most standard NFIP policies exclude finished basements and personal property stored below the lowest adjacent grade. Basement-specific exclusions mean items like carpeting, drywall, and furnishings below grade typically aren't covered. Check your specific policy and consider excess flood insurance for additional basement protection.

Does flood insurance cover water damage from a burst pipe?

No. Flood insurance specifically covers direct physical damage from external floodwaters, rain, storm surge, or overflowing rivers. Water damage from a burst pipe, plumbing failure, or internal water backup is considered a maintenance issue and is typically covered under homeowners insurance instead. Understanding this distinction helps you maintain appropriate coverage through both policies.

How long is the waiting period for flood insurance to take effect?

The standard flood insurance waiting period is 30 days from the date your policy is issued. This means coverage doesn't begin until 30 days have passed. However, if you're purchasing flood insurance as a requirement for a mortgage, the waiting period may be waived. Always confirm your specific policy's waiting period with your insurance agent to understand when protection begins.

What happens after I file a flood insurance claim?

After filing a claim, an adjuster will assess the damage and determine coverage based on your policy limits and deductible. You'll need to provide proof of loss, including photos and documentation of damaged items. Post-flood mitigation requirements may apply, you must take reasonable steps to prevent further damage. The claims process timeline varies, but insurers typically work to resolve claims within 30-60 days, depending on damage severity.