Table of Contents

- What Does Renters Insurance Cover in Nevada?

- Nevada-Specific Perils Every Renter Should Know

- Landlord Insurance vs. Tenant Insurance: Where the Line Is Drawn

- Renters Insurance Personal Property Coverage Limits Explained

- Is Renters Insurance Mandatory in Nevada?

- Average Cost of Renters Insurance in Nevada

- How to File a Renters Insurance Claim in Nevada

- What Does Renters Insurance Cover in Nevada: Choosing the Right Policy

Last Updated: June 16, 2026

Renters across Nevada often assume their landlord’s insurance policy covers their belongings. It does not. Understanding what does renters insurance cover in Nevada is one of the most important financial decisions a tenant can make, and this guide from United Family Insurance breaks down every coverage type, Nevada-specific risk, and policy detail you need to know before signing up or filing a claim.

Nevada’s climate, legal environment, and urban density create coverage needs that differ meaningfully from other states. Below, we’ll show you exactly how each coverage type works, where landlord policies end and yours begins, and how to build a policy that actually protects you in Las Vegas or Reno.

What Does Renters Insurance Cover in Nevada?

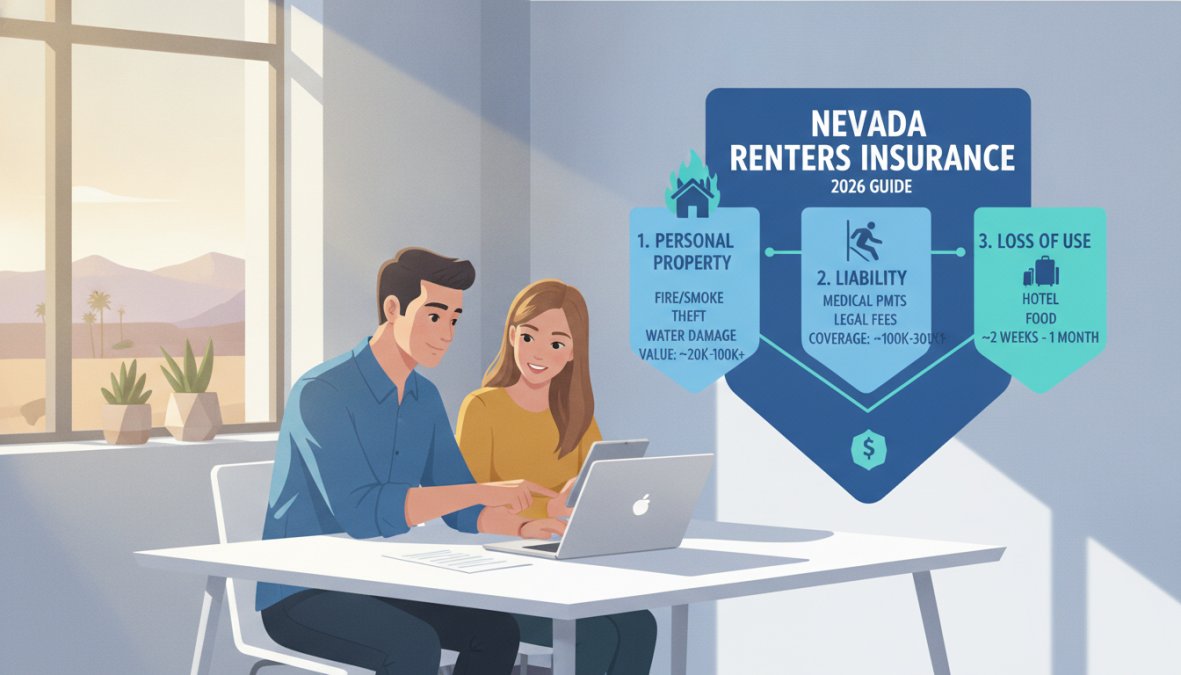

Renters insurance in Nevada protects tenants against financial loss from covered perils, personal liability claims, and temporary displacement costs. A standard policy bundles four core protections: personal property, personal liability, loss of use, and medical payments to others.

Personal Property Protection

Personal property coverage pays to repair or replace your belongings when damaged or destroyed by a covered peril, fire, theft, vandalism, smoke, burst pipes, or windstorm. Your furniture, electronics, clothing, and appliances all qualify.

Most people underestimate what they own. Walk through each room and total what it would cost to replace everything; the number is usually higher than expected. Entry-level policies may set limits as low as a few thousand dollars, so choosing the right limit starts with an honest home inventory, covered later in this guide.

Personal Liability Coverage

Personal liability coverage protects you if someone is injured in your rental or if you accidentally damage others’ property. If a guest slips and sues you, liability coverage pays legal defense costs and any settlement up to your policy limit. It often extends beyond your unit, if your dog bites someone at a park, your liability coverage may apply. Standard limits are moderate; tenants with significant assets should consider higher limits or an umbrella policy.

Many tenants assume a landlord’s liability insurance covers guest injuries inside the unit. It does not. Landlord policies cover the building and the landlord’s liability, not yours. Without renters insurance, you pay legal costs out of pocket.

Loss of Use and Additional Living Expenses

Loss of use coverage pays for temporary housing and related costs when your rental becomes uninhabitable due to a covered loss. If a kitchen fire forces you out of your Las Vegas apartment for three weeks, this coverage handles hotel bills and meals above your normal food budget. Policies carry both a time limit and a dollar cap, know both before disaster strikes. Even modest Las Vegas hotel stays add up quickly, so a higher loss of use limit is worth the marginal premium increase.

Medical Payments to Others

Medical payments coverage (MedPay) pays minor medical expenses if a guest is injured on your property, regardless of fault. Unlike liability coverage, it requires no lawsuit or proof of negligence, it handles smaller claims quickly and prevents disputes from escalating. Think of it as a goodwill layer for immediate costs, while liability coverage handles larger legal claims.

Nevada-Specific Perils Every Renter Should Know

Nevada’s geography creates risks that standard insurance guides rarely address. Renters in Las Vegas, Henderson, and Reno face extreme heat, dust storms, and flash flooding that can cause serious property damage in short periods.

Heat, Dust Storms, and Flash Flooding in Las Vegas and Reno

Extreme summer heat accelerates HVAC wear and can cause pipes to fail in ways that trigger water damage claims. According to Nevada Division of Emergency Management’s hazard mitigation resources, flash flooding is one of the most significant natural hazards facing Nevada communities, particularly in the Las Vegas Valley where desert terrain channels water rapidly. Haboobs can force fine particulate matter into apartments and damage electronics; standard policies cover sudden and accidental damage, but gradual dust infiltration is typically excluded.

Flash flooding is a critical coverage gap. Water damage from a burst pipe is covered; water damage from a flash flood is not. Nevada renters near washes, arroyos, or low-lying areas should evaluate a separate flood insurance policy through the National Flood Insurance Program.

What Standard Policies Do Not Cover in Nevada

Knowing your exclusions is as important as knowing your coverage. Standard renters insurance in Nevada does not cover:

- Flood damage (requires separate flood insurance)

- Earthquake damage (requires a separate endorsement or policy)

- Pest infestations, including scorpions and cockroaches common in southern Nevada

- Normal wear and tear on belongings

- Intentional damage caused by the policyholder

- High-value items above scheduled limits without a rider or floater

Earthquake exclusions deserve particular attention, Nevada sits in a seismically active region. Ask specifically about an earthquake endorsement when shopping for coverage.

If you live near a Las Vegas Valley wash or in a low-elevation neighborhood in Reno, request a flood zone determination from your [insurance agent](/benefits-of-using-an-independent-insurance-agent/) before finalizing your policy. Flood risk in Nevada is underestimated by many renters until the first monsoon season.

Landlord Insurance vs. Tenant Insurance: Where the Line Is Drawn

Landlord insurance covers the physical structure, the landlord’s personal liability, and lost rental income if the property becomes uninhabitable. It does not cover a tenant’s personal property, liability, or additional living expenses.

| What Happened | Covered by Landlord Insurance | Covered by Renters Insurance |

|---|---|---|

| Fire damages building structure | Yes | No |

| Fire destroys your furniture | No | Yes |

| Guest injured in your unit sues you | No | Yes (your liability) |

| Guest injured in common area sues landlord | Yes | No |

| Pipe bursts, damages building | Yes | No |

| Pipe bursts, damages your laptop | No | Yes |

| You must temporarily relocate | No | Yes (loss of use) |

The boundary is clear: the landlord owns the building; you own everything inside your unit. Any financial exposure tied to your belongings or your actions is yours to manage with a renters policy.

Renters Insurance Personal Property Coverage Limits Explained

Coverage limits define the maximum your insurer will pay for a covered loss. Choosing the wrong limit is one of the most common and costly mistakes renters make.

Actual Cash Value vs. Replacement Cost: Which Should You Choose?

Actual cash value (ACV) pays after accounting for depreciation, if your three-year-old laptop is stolen, ACV pays what it’s worth today, not what a new one costs.

Replacement cost value (RCV) pays the full cost to replace the item with a new equivalent, regardless of depreciation. RCV costs more in premium, but the payout difference on a significant claim can be substantial.

For most Nevada renters, replacement cost coverage is the better choice. The premium difference is usually modest, and the financial protection in a major loss is meaningfully greater. ACV policies make sense primarily for renters whose belongings’ depreciated value closely matches replacement cost.

How to Build a Home Inventory in Nevada

A home inventory is a documented record of your belongings used to support insurance claims. Without one, proving the value of lost or damaged items becomes difficult and disputes with insurers are more likely.

Home Inventory Checklist:

- Walk through each room and photograph or video all belongings

- Record item descriptions, purchase dates, and estimated values

- Photograph serial numbers on electronics and appliances

- Save receipts for high-value purchases in a digital folder

- Note any items that may require a scheduled personal property rider (jewelry, art, collectibles)

- Store your inventory file in cloud storage or an off-site location, not just on a local device

- Update the inventory annually or after major purchases

Nevada renters with high-value items like gaming equipment, musical instruments, or jewelry should ask about scheduled personal property endorsements, as standard policies cap payouts on specific categories.

Building a home inventory takes about two hours for a typical apartment. That two-hour investment can save thousands of dollars in a disputed claim. Store it somewhere accessible outside your home.

Is Renters Insurance Mandatory in Nevada?

Renters insurance is not legally required by Nevada state law. However, many landlords in Las Vegas and Reno include it as a lease requirement, failing to maintain coverage is a lease violation that could result in eviction. Always confirm whether your landlord requires proof of renters insurance before move-in.

Beyond lease requirements, the Nevada Revised Statutes hold tenants financially liable for damage they cause. Without a renters policy, that liability comes directly out of your pocket. The Nevada Revised Statutes on landlord-tenant law outline tenant obligations that make liability coverage a practical necessity even when not legally required.

Average Cost of Renters Insurance in Nevada

Renters insurance in Nevada is generally among the more affordable personal insurance products available. United Family Insurance compares the market on your behalf, surfacing quotes from multiple carriers in a single step rather than requiring hours of individual shopping.

Key Factors That Affect Your Premium

- Coverage limits: Higher personal property and liability limits increase your premium.

- Deductible: A higher deductible lowers your monthly premium but increases out-of-pocket cost at claim time.

- Location: Areas with higher crime rates or flood risk, such as certain Las Vegas neighborhoods, may cost more.

- Claims history: Prior claims can raise your premium.

- Coverage type: Replacement cost policies cost more than actual cash value policies.

- Additional riders: Scheduled personal property endorsements and earthquake riders add to the base premium.

- Bundling discounts: Combining renters insurance with auto insurance often reduces both premiums.

Raising your deductible is the fastest way to lower your premium, but choose an amount you could comfortably pay from savings in an emergency.

How to File a Renters Insurance Claim in Nevada

Filing a claim efficiently depends on preparation. Most claims that get delayed or disputed do so because of missing documentation, not insurer bad faith.

Step 1: Ensure Safety First

Confirm the situation is safe. For fire or structural damage, wait for clearance from emergency services.

Step 2: Document Everything

Photograph and video all damage before touching or moving anything. Capture wide shots and close-ups of every affected item.

Step 3: File a Police Report if Applicable

For theft, vandalism, or any criminal incident, file a police report immediately. Your insurer will require the report number.

Step 4: Contact Your Insurer

Report the claim as soon as possible. Provide your policy number, a description of the incident, and your documentation.

Step 5: Complete the Proof of Loss

Your insurer will request a formal proof of loss statement listing all damaged or stolen items with their values. Your home inventory makes this step significantly faster.

Step 6: Work with the Claims Adjuster

An adjuster will review your claim and assess the damage. Be present during the inspection if possible and ask questions about anything unclear.

Step 7: Receive Your Settlement

Once approved, your insurer issues payment minus your deductible. For replacement cost policies, some insurers pay ACV initially and release the remaining amount once you purchase replacements.

According to the Insurance Information Institute’s guidance on filing claims, keeping thorough records throughout the claims process is the single most effective way to ensure a fair and timely settlement.

Do not dispose of damaged items before your adjuster inspects them. Disposing of evidence before the inspection can result in your claim being denied or reduced significantly.

What Does Renters Insurance Cover in Nevada: Choosing the Right Policy

Selecting the right renters policy comes down to three decisions: coverage type (ACV vs. replacement cost), coverage limits that match your actual property value, and any riders needed for high-value items or Nevada-specific perils like earthquakes.

The biggest gap in most renters policies is not the standard coverages, it is the exclusions. Flood and earthquake coverage require separate action in Nevada, and most renters only discover this after a loss. Addressing those gaps at policy inception costs far less than facing an uninsured loss.

For Las Vegas renters, the combination of flash flood risk, extreme heat, and urban theft rates makes a comprehensive policy with strong liability limits and replacement cost coverage the most defensible choice. Reno renters face similar earthquake and flood exposure and should evaluate the same additions. The difference in premium between a bare-minimum policy and a well-structured one is often smaller than most renters expect.

The Nevada Division of Insurance consumer resources provides additional guidance on tenant rights and insurance requirements for Nevada residents.

Choosing the right renters insurance in Nevada is not complicated, but the cost of getting it wrong is real. United Family Insurance compares the market on your behalf, connecting you with affordable, comprehensive coverage options from multiple carriers without the hours of individual shopping. Our expert agents provide guidance on Nevada-specific risks, coverage limits, and endorsements so your policy reflects your actual needs. Get a quote from United Family Insurance and secure the financial protection your Las Vegas or Reno rental deserves.

Frequently Asked Questions

Is renters insurance required by law in Nevada?

Nevada state law does not legally require renters to carry renters insurance. However, many landlords in Las Vegas, Reno, and other Nevada cities include a renters insurance requirement in the lease agreement. If your lease requires it, failing to maintain a policy could be considered a lease violation. Even when it is not mandatory, carrying a renters policy is strongly advisable to protect your personal property and liability exposure.

Does renters insurance cover water damage in Nevada?

A standard renters insurance policy in Nevada typically covers sudden and accidental water damage, for example, a burst pipe or an overflowing appliance, that damages your personal property. However, it generally does not cover flood damage caused by rising groundwater or flash floods, which are a real risk in areas like Las Vegas. For flood protection, renters need a separate flood insurance policy through the National Flood Insurance Program or a private insurer.

How much does renters insurance cost in Nevada on average?

Renters insurance in Nevada is generally considered affordable, with monthly premiums varying based on your location, coverage limits, deductible, and the value of your personal property. Factors like living in a high-crime ZIP code in Las Vegas or selecting replacement cost coverage instead of actual cash value can raise your premium. Shopping the market and comparing multiple quotes is the most effective way to find a policy that balances comprehensive coverage with an affordable price.

Does renters insurance cover theft outside of my apartment in Nevada?

Yes, most standard renters insurance policies extend personal property coverage beyond your apartment walls. If your belongings are stolen from your car, a hotel room, or even while you are traveling, your renters policy may cover the loss up to your policy limits and minus your deductible. High-value items like jewelry or electronics may have sub-limits, so consider adding a rider or scheduled personal property endorsement for full protection.

What is typically not covered by a standard Nevada renters insurance policy?

Standard renters insurance in Nevada does not cover flood damage, earthquake damage, your roommate's belongings (unless they are listed on the policy), or damage you intentionally cause. It also excludes pest infestations and general wear and tear. Vehicles are covered under auto insurance, not your renters policy. If you run a business from home, business equipment may have limited coverage. Riders and endorsements can fill some of these gaps depending on your insurer.

How do I file a renters insurance claim in Nevada?

To file a renters insurance claim in Nevada, start by documenting the damage or loss with photos and a written inventory of affected items. Report the incident to local authorities if theft or vandalism occurred and obtain a police report number. Then contact your insurance agent or carrier promptly, provide all documentation, and complete the required claim forms. Keep records of all communications and any temporary living expenses if you are displaced, as these may be reimbursable under your loss of use coverage.